Welcome to a new section of the newsletter that will be home to the MIA Model Portfolio. This is an experimental virtual portfolio with a trading strategy based on the MIA Ratings and the MIA Sentiment Index.

I created the MIA Ratings to help with my investment decision making process and use them alongside additional research to try and make objective investment decisions. But occasionally emotion creeps in. I might get over enthusiastic about my latest investment idea or decide to keep those losing investments for just one more RNS…

For this experiment I am going to eliminate emotional bias by removing myself from any decision making. All trades will be automated with decisions based purely on the trading strategy outlined below.

Asset Allocation

The portfolio will consist of UK listed shares and will be benchmarked against the SPDR FTSE UK All Share Accumulation ETF (FTAL) as a proxy for the FTSE All Share Total Return Index. The initial portfolio value will be £10,000.

Cash

The cash level will to a large extent be determined by the trading strategy described below, but there will also be a target cash allocation that will be linked to the level of the MIA Sentiment Index. Only excess cash held above the current target allocation will be made available for trading.

The relationship between the cash allocation target the MIA Sentiment Index is non-linear. In practice this means that progressively larger amounts of cash held in the portfolio will be released for trading for each unit of downward movement in the MIA Sentiment Index.

In order to avoid buying into rapidly falling markets, access to cash held in the portfolio will be locked during large downward movements in the MIA Sentiment Index.

Equities

The target allocation for an individual holding will be based on its overall MIA Rating score in relation to the ratings of each of the other holdings in the portfolio. Target allocations are therefore expected to be quite fluid, changing with the movements of the MIA Ratings scores.

Trading Strategy

The initial criteria for different types of trade are set out below. These may evolve over time as trading and performance histories are built up and analysed.

Buy Strategy

A stock will be given a ‘Buy’ rating if its MIA Rating scores for Quality, Value, Safety Margin, and Outlook are all in the top quartile of the scores of stocks in MIA investment universe.

A ‘Buy’ rating will only be acted upon if there is excess cash above the current cash allocation target to cover the trade.

In order to ensure a minimum level of diversification, a limit will be placed on the value of each ‘Buy’ trade so that the purchased holding does not exceed 10% of the portfolio following the transaction.

Top Slice Strategy

The initial top slicing policy will be designed to manage single stock risk arising from overweight positions. Each holding will be allowed to drift up to a fixed percentage above its target allocation before being top sliced.

Sell Strategy

A position will be sold if its MIA Rating scores for either Quality or Outlook fall below the top quartile of the scores of all stocks in MIA investment universe.

Initial Trades

The portfolio was launched on 4th January 2022, the first trading day of the year. The following trades have been made so far.

AJ Bell (AJB)

Buy: Price 387.8p / Book Price 393.7p

AJ Bell was the first addition to the portfolio. I highlighted AJ Bell’s quality metrics when I wrote about the company back in October. The shares also had the highest MIA Share Ranking in December.

The shares were purchased on a trailing price to earnings of ~36 times. At the time of purchase this was close to a 3 year low, but still a premium valuation in absolute terms.

The sell off in small and mid caps in the first few weeks of the year has seen the share price slip back further since this transaction and is currently at its lowest level since April 2020. The share price has now fallen below the trading range of its longer term consolidation phase.

Fidelity China Special Situations (FCSS)

Buy: Price 304.0p / Book Price 308.6p NAV Discount: -4.9 %

Negative news flow made China an unpopular investment in 2021. The share price of this fund peaked at ~500p in February last year and has been heading downwards ever since. At the time of this transaction the share price was at a 52 week low and at a wider discount to NAV than the 12 month average.

The negative news may have kept investors away but managers of funds that have a large exposure to China have not appeared overly alarmed about navigating the stricter regulatory environment or developments in the real estate sector.

FCSS manager Dale Nichols made the point in a recent newsletter that the “key thing will be individual companies’ ability to deliver on their earnings potential over time”. Corporate earnings in China are forecast to grow by more than 15% over the next 12 months.

Molten Ventures (GROW)

Buy: Price 914.0p / Book Price 928.0p

Another thematic choice for the portfolio is European technology venture capital firm Molten Ventures, formerly Draper Esprit. The recent re-brand coincided with a move from AIM to the main market in 2021.

The 70+ underlying holdings offer high growth potential, but also high risk. The core portfolio is fairly concentrated with 17 companies accounting for 68% of holdings. The interim results at the end of November had a bullish outlook:

“…portfolio growth is already well ahead of our stated financial objective of 15% Gross Portfolio fair value growth for this financial year, and our portfolio continues to perform strongly. We therefore anticipate fair value growth in the region of 35% for the full year to 31 March 2022, subject to wider market conditions.”

Frontier Developments (FDEV)

Buy: Price 1350p / Book Price 1364p

Frontier Developments appeared in both the MIA Ratings November Top 3 and the December Top 5. The share price has since taken another tumble following the company’s January trading update.

The recently launched Jurassic World Evolution 2 had a ‘‘strong second month of sales” following an initially poor sales performance on PC at release. Sales achieved nearly 1 million units in the first 9 weeks since release. It’s predecessor, by comparison, achieved sales of 1 million units in just 5 weeks. The release of the original game did coincide with the release of the Jurassic World: Fallen Kingdom film which would have helped sales. The latest film in the franchise, Jurassic World: Dominion, is due for release in June 2022 which should give Evolution 2 a mid year sales boost.

The trading update also indicated that the planned release date of the future Warhammer: Age Of Sigmar game would now be pushed backed to FY24, impacting FY23 revenues.

Notwithstanding the recent disappointing trading updates, the longer term outlook remains positive. The 2022 calendar year should start to see Frontier’s 3rd party publishing label, Frontier Foundry, being scaled up and the release of a new F1 Management game.

Allianz Technology Trust (ATT)

Buy: Price 288.5p / Book Price 292.9p NAV Discount: -9.74 %

The Allianz Technology Trust is a global technology fund but the portfolio is heavily weighted to the US. This fund has an excellent track record, outperforming its benchmarks (and the FTSE World TR) over 3, 5, and 10 years.

Recent negative sentiment amid a sell off of US technology stocks has left this fund at a significant discount to NAV, presenting an opportunity to buy. The long term outlook for US technology continues to be attractive.

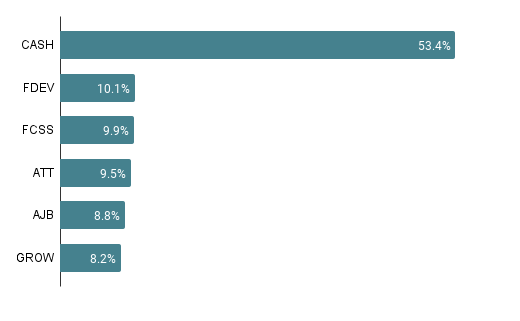

Portfolio Composition

In each of the initial trades, the maximum permitted allocation of 10% of the portfolio value was acquired, leaving approximately 50% in cash. The current portfolio composition is shown below:

It’s been a difficult market environment for the first few weeks of the portfolio. Recent negative sentiment resulted in AJ Bell and Molten Ventures both falling significantly after acquisition accounting for most of the portfolio performance of -4.9% YTD. Maybe not the best start, but the limit on acquisition weightings combined with the large unallocated cash position may have prevented it from being much worse. Below are the contributions to the total return so far.

The portfolio benchmark, the FTSE All Share Total Return Index, is roughly flat YTD (from the 2021 closing price), but the market story so far this year is best illustrated by looking at its constituent indices. The FTSE 100 slightly up, but the FTSE 250 is down by almost -8%. The AIM All Share Index is also down by around -11%.

Continued negative sentiment towards FTSE 250 stocks could see the portfolio value fall further, but might also present some further buying opportunities. Whatever happens, it will be interesting to see how the portfolio develops and to analyse what went right and what went wrong along the way.

Thanks for reading, and I wish you all a successful year of investing in 2022.

This article is intended for informational purposes only. It is not a recommendation to buy or sell shares or other investments. Always do your own research before buying or selling any investment or seek professional financial advice.