In the cloud, everything is seamless. On any device, in any location, at any time, we can connect to our familiar environment and pick up right where we left off.

In the new world of hybrid/remote working it’s the cloud that enables employees to work from home, the office, or anywhere else. The cloud is also changing the way that customers can (and want to) interact with businesses, moving away from just phone calls to multiple contact channels that include email and web chat.

AIM listed Gamma Communications (GAMA) provides the communication infrastructure and services that enable businesses to support these trends. It’s key strategic products include SIP Trunking (an alternative to a traditional phone line enabling Voice over IP calls), and Horizon, a cloud based telephony (or PBX) system, which the company is evolving into a full Unified Communications as a Service (UCaaS) product that includes instant messaging, video calls, and conference services.

MIA Ratings

Here’s the scorecard from the MIA Stock Report for Gamma Communications at the time of writing:

The scores suggest that Gamma has some quality financial metrics, has had some recent negative sentiment, and has a positive long term outlook. In the following sections I’ll take a look at some of the factors driving the scores in each category.

As always, the scores shouldn’t be relied upon to make any investment decisions.

Financials

The first thing that stands out from the financials section of the MIA Stock Report is that Gamma’s earnings are very high quality. The company generates most of its revenue through subscription based services and regularly achieves recurring revenue levels in excess of 90%.

Gamma also scores highly for Return on Capital Employed (which is in excess of 30%), often the mark of a high quality business. The operating margin scores look interesting and could be worth investigating further. The relatively low score in the efficiency section implies that a high capital turnover is required to generate that high ROCE, but margins are also growing strongly. We can take a look at some data to see what’s happening. The charts below show Gamma’s operating margins and capital turnover for the last five years:

Gamma’s operating margins actually look pretty healthy and the score of 24 on the report is perhaps a bit harsh. The margins have also been steadily increasing as the scores suggested, while capital turnover is reasonably high but has fallen to around 2 over the last couple of years.

To understand why margins are increasing we need know more about Gamma’s full product range and the trends taking place in the communications market.

Gamma provides services across voice, data, and mobile. Those services include traditional phone lines and call packages, broadband, and mobile phone packages. The key growth drivers of Gamma’s business though are it’s cloud based SIP Trunking (VoIP) and Horizon Cloud PBX/UCaaS products which have higher margins than Gamma’s other products.

As businesses transition to cloud based communications, Gamma’s sales mix is becoming more weighted towards its higher margin cloud products, driving up it’s overall margin. Increasing margins also enable profit to grow faster than revenue, giving the business operational gearing. The effect of this can be seen in the chart below which shows that Gamma’s operating profit growth has been consistently higher than revenue growth over the last few years:

The decrease in capital turnover shown in the earlier chart can at least in part be attributed to Gamma’s expansion into Europe which began in 2018 through a number of acquisitions. The acquisitions significantly increased the level of capital employed in the business and introduced a certain amount acquisition related intangible assets, the effect of which is a reduction in capital turnover. Regardless of this, ROCE remains high, helped by those increasing margins. Gamma sees a big market opportunity in Europe and its very likely that there will be more European acquisitions in the pipeline.

Valuation And Margin Of Safety

Gamma generally has mid range scores for valuation suggesting that the shares are probably fairly valued at their current price. The margin of safety report shows an extremely high score for recent downside volatility which calls for a look at the share price chart:

As suspected, Gamma shares recently experienced a sharp sell off from an all time high after the company released its half year results in September. The shares fell by ~22%, and are now consolidating at around 1830p. The share price drop looks to initially have been profit taking, reversing some over enthusiasm for the shares triggered by the preceding positive trading update in July. A broker downgrade issued a week after the release of the half year results triggered further selling.

The half year results reported “growth across all key product categories” with revenue and operating profit increasing by 23% and 25% respectively compared to the previous year. Full year results are expected to be in line with market expectations.

Outlook

Cloud Based Communications Market

Market Trends

The transition to cloud based communications services has been taking place in the UK for a number of years and is expected to accelerate post pandemic. Businesses will need to provide multiple communication channels to support both their internal operations and their customer contact preferences.

Market Opportunity

Gamma sees the transition to cloud based communications as a significant market opportunity. The 2021 Annual Report notes that:

The market opportunity of adoption is still mainly untapped across the UK and European markets that Gamma operate in, with less than 30% market adoption even in the most “advanced “ countries.

One of those most “advanced“ countries is the UK - Gamma’s core market from which it currently generates 88% of revenues. It’s useful to look at how the UK market has evolved to see where the future market opportunity lies for Gamma. The charts below show the evolution of the UK markets for Gamma’s key strategic products of SIP Trunking (VoIP) and cloud based PBX/UCaaS systems and nicely illustrate how they fit into different market phases.

In both charts, the light grey bars indicate the market opportunity. The gold and purple bars show the market adoption.

The chart on the left shows the initial market phase where businesses transitioned from traditional ISDN telephone lines to basic VoIP systems. These are now widely adopted with the market approaching saturation. Traditional telephone networks are in fact now beginning to be switched off across Europe in favour of IP based systems. In the UK this is planned to happen in 2025.

The chart on the right illustrates the next market phase where businesses move from basic VoIP to fully cloud hosted telephony (PBX) systems. Market adoption in the UK is currently around 30%. Over time this market is expected to evolve from cloud hosted telephony into full featured UCaaS systems that support multiple communication channels (currently this is only a tiny fraction of the data included in the chart).

European markets are expected to follow a similar path to that in the UK, but are mostly at a much earlier stage in their development. Gamma has market leading positions in the UK and has identified Europe as a significant opportunity to replicate that success.

Strategy

Gamma’s product strategy is to focus on the expected market evolution from VoIP to cloud hosted PBX services and then to the adoption of UCaaS by evolving its existing Horizon cloud telephony service into a full featured UCaaS offering.

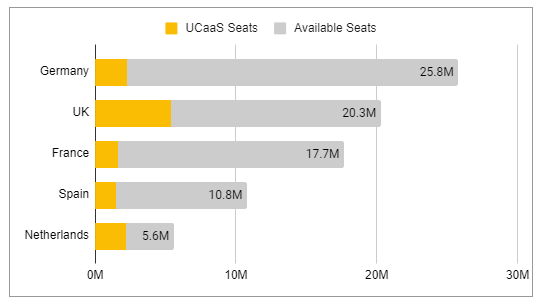

The company’s growth strategy is to take advantage of the current low market adoption and expected growth of cloud based communication services, and to massively increase its addressable market through expansion into Europe. To give you an idea of the scale of the European opportunity for Gamma, the UK has ~20 million potential cloud PBX/UCaaS seats (or billable units). Western Europe has a potential ~123 million seats with about 16% market adoption (much lower in some countries). The chart below shows the potential market sizes (grey) and current market adoption (yellow bars) in different European countries.

Gamma’s recent acquisitions mean that it currently has a presence in Germany, Spain, and the Netherlands in addition to the UK.

Culture Deteriorating?

Gamma’s strategy of expansion into Europe was initiated in 2018 when CEO Andrew Taylor took the helm. The change of leadership may also have been the catalyst for a cultural shift within the organisation.

Prior to 2018 the company consistently placed in the top 50 of the “Sunday Times 100 Best Companies to Work For” list, each time achieving a 2 star accreditation. In 2018, under the new CEO, the company achieved a 1 star accreditation and didn’t disclose it’s list placing in it’s Annual Report - but did restate the position it had achieved the previous year.

In 2019 the company again achieved a 1 star accreditation and disclosed that it placed 87th in the list. The 2020 Annual Report did not mention the “Sunday Times 100 Best Companies to Work For” list at all. The table below documents Gamma’s slide down the Sunday Times list:

There is also a change in messaging in the latest Annual Reports. The Social Governance sections of the reports from 2015 - 2018 have people focused headlines (e.g. “People Power“, “Celebrating the Power of People“), and they all open with the line:

Our culture has been instrumental in the growth and success of the business to date.

Compare with the 2019 Annual Report’s Social Governance section which has the much more corporate sounding headline, “Gamma takes the welfare of its stakeholders very seriously”, and opens with:

We … focus on working with our stakeholders... We identify these as our customers, suppliers and our people.

That’s customers first, then suppliers, then people.

The 2020 Annual Report does say that during the year the company launched a new set of values, introduced a new employee engagement tool (called Gamma Pulse) and has created a “senior leaders engagement working group to help drive change and actions in the business”.

Gamma currently has market leading positions in the UK cloud communications market, and culture would very likely have played a part in helping it to achieve that success. The company will be facing increasing competition as it expands into Europe and needs to ensure that its culture is not eroded if it is going to repeat its UK success in its new target markets.

This article is intended for informational purposes only. It is not a recommendation to buy or sell shares or other investments. Always do your own research before buying or selling any investment or seek professional financial advice.