Macro factors took precedence over fundamentals during the second quarter as inflation raced ahead and central banks increased interest rates. Consequently growth stocks continued to de-rate as the present value of their future earnings fell.

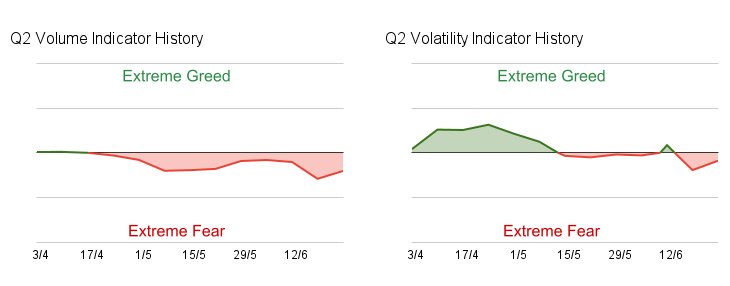

Many growth stocks have now fallen by 50% or more since the start of the year, but so far there hasn’t been market capitulation characterised by high volumes and a spike in volatility. The charts below track the volume and volatility indicators of the MIA Sentiment Index over the quarter:

Sentiment then has been largely driven by steady but unexceptional selling volumes. The anticipated mid-June increase in interest rates had a small and short-lived effect on the sentiment indicators shown by the dip on the far right hand side of each chart. The MIA Sentiment Index closed the quarter comfortably in the ‘Fear’ range at 35, but so far has not dropped into the ‘Extreme Fear’ range in the year to date.

Portfolio Holdings

At the end of Q2 the portfolio continued to hold a large cash position, providing some much needed capital preservation:

This is an experimental virtual portfolio with a trading strategy based on the MIA Ratings and the MIA Sentiment Index. All trades in the model portfolio are automated according to the rules outlined in this post.

Positions in Fidelity China Special Situations (FCSS) and Molten Ventures (GROW) were exited during the quarter following their FY results and a reassessment of their medium term outlooks. The funds were redeployed into Impax Asset Management (IPX) and Alpha FX Group (AFX). While I’m hopeful that these will both prove to be good long term holdings, they may well have been acquired too early in a falling market and I might tighten the capital preservation strategy a little.

Performance

The portfolio fell by -12.3% in Q2 and is now down -17.8% YTD. The chart below shows the YTD portfolio performance compared to the SPDR FTSE UK All Share Accumulation ETF (FTAL) as a proxy for the FTSE All Share Total Return index. The large caps of the FTSE 100 continue to prop up the FTSE All Share. For comparison the FTSE 250 is down by ~22%.

Frontier Developments (FDEV) was the main positive contributor to performance during the quarter helped by a share price rise of ~43% in the week following its positive June trading update. The shares have fallen back a little since, and the impact of positive news on the share price may prove to be short lived as has been the case with many shares so far in 2022.

The return contributions from each of the holdings during the quarter are shown below:

Summary

It seems likely that the macro environment will continue to have a significant influence over the portfolio’s performance for the remainder of the year. So far we have seen significant price contraction with little impact on reported earnings. If earnings contraction is to follow, it could provide the trigger for market capitulation that has been missing from the current downturn.

Capitulation might also trigger the deployment of more cash from the portfolio. For now though the cash balance is welcome and is just about containing the losses to a level that can be recovered by a similar sized gain.

This article is intended for informational purposes only. It is not a recommendation to buy or sell shares or other investments. Always do your own research before buying or selling any investment or seek professional financial advice.