The volatility and sharp downside movements in markets during the first quarter of 2022 was perhaps not the easiest of environments in which to launch a new portfolio, particularly with a trading strategy that favours growth stocks. Sentiment towards stocks in the MIA investment universe measured by the MIA Sentiment Index reached low points at the end of January, and at the beginning of March in the week following Russia’s invasion of Ukraine. The charts below track the change in sentiment over the quarter.

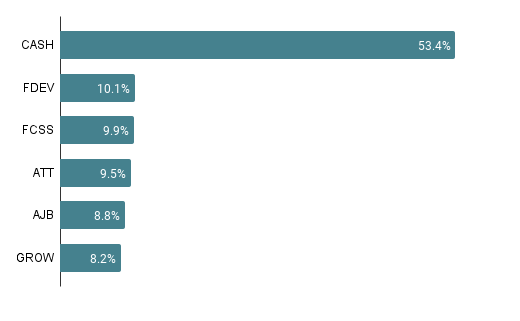

After a flurry of initial purchases made in January, the portfolio consisted of 5 holdings with just over 50% still in cash:

The share prices of each of the new holdings had already fallen significantly at the time they were acquired, but there were further significant falls to come as inflationary fears took hold and growth stocks continued to be sold off. The initial allocation sizes and the constraints of the automated trading strategy meant that averaging down was not considered for any of the holdings as their share prices fell. Here’s a quick reminder of the purchase criteria:

A stock can be acquired if its MIA Rating scores for Quality, Value, Safety Margin, and Outlook are all in the top quartile of the scores of stocks in MIA investment universe, and if the purchase does not result in the holding allocation exceeding 10% of the portfolio value.

One additional position was taken in Smithson (SSON) in February. At 1582p, the shares had fallen by more than 20% from their peak at the start of year. This investment trust very rarely trades at a discount and the shares were acquired at a price approximately equivalent to NAV. Smithson, like its sibling Fundsmith, invests in companies that should have high enough margins and pricing power to be able to cope relatively well in the current economic environment, but time will tell. In his annual letter to shareholders in February, Smithson manager Simon Barnard highlighted the potential for the fund to underperform if inflation proves not to be transitory:

we […] consider ourselves fortunate to have outperformed in this environment, and if this trend of increasing interest rate expectations persists, we may not continue to be so lucky.

Following the Smithson purchase the portfolio ended the quarter with the following allocations:

Portfolio News And Commentary

The full year results for the Allianz Technology Trust were released in March, revealing that the fund underperformed its benchmark, The Dow Jones World Technology Index, by 8.8% in 2021, but still increased its NAV by 19.4%. This compares with an outperformance of 34% the previous year. This investment trust tends to favour higher growth stocks and has an underweighting to the tech mega-caps. Hopefully that gives it the potential to outperform over the longer term. Also of note is news that the investment manager, Walter Price, will be handing over to long term colleague Mike Seidenberg in July 2022. The investment approach is not expected to change, but it’s something to keep an eye on.

Coinciding with the start of the new Formula 1 season, Frontier Developments began trailing its new F1 Manager game due to be released this summer, and also announced new games releases from it’s 3rd party publishing label, Frontier Foundry, during the quarter. The annual updates to F1 Manager and scaling up of Frontier Foundry should both help to smooth Frontier’s revenue stream over the next few years, reducing its reliance on the success of new blockbuster titles.

Fidelity China Special Situations continued to sell off following its addition to the portfolio in early January with investors staying away from Chinese stocks after the government’s regulatory interventions in 2021. In mid March there came news of a possible change in stance from Beijing, triggering a day of frantic buying, but investors will need to see actions rather than words for sentiment towards Chinese stocks to turn around. If that happens, the price of this fund could rise rapidly.

The share price of Molten Ventures, another early January portfolio addition, has been hit particularly hard. In the first week of March the shares were trading more than 50% below their peak from September last year. Updates from Molten released in February and March remained bullish and both reiterated the previous guidance of 35% fair value growth of the portfolio for FY22. CEO Martin Davis said in the February update:

The European technology venture market continues to thrive despite the wider fluctuations in public markets and demonstrates the uncorrelated nature of public and private markets in this space. Molten is well-positioned to take advantage of this disconnect and our year end guidance of fair value growth in the region of 35% remains, keeping up the strong momentum we evidenced so far this year.

An Edison Research Note also released in February estimated that this would translate to a FY22 NAV per share of 929p. That implies the initial portfolio purchase in January at 914p was made at a premium to NAV of a few percent. Since then the shares have traded as low as 611p - a significant discount to the estimated FY22 NAV for anyone brave enough to purchase.

A January trading update from AJ Bell, indicated continued growth in customer numbers and assets under administration (AUA), the key drivers of its business, with CEO Andy Bell commenting:

We continue to see strong demand for our easy to use, low-cost platform across both the advised and direct-to-consumer markets.

This didn’t halt a share price slide that was already well underway, and shares in AJ Bell are now trading at prices last seen at the height of the pandemic in March 2020.

Portfolio Performance

The portfolio fell by -6.3% in the quarter. The chart below shows the performance compared to the SPDR FTSE UK All Share Accumulation ETF (FTAL) as a proxy for the FTSE All Share Total Return index. The FTSE All Share, heavily weighted by the large caps of the FTSE 100, has had a resilient quarter. The same can’t be said for the FTSE 250 (down by ~10% ) or the AIM All Share (down by ~14%) which perhaps demonstrates the breadth of the sell off across small cap and growth stocks.

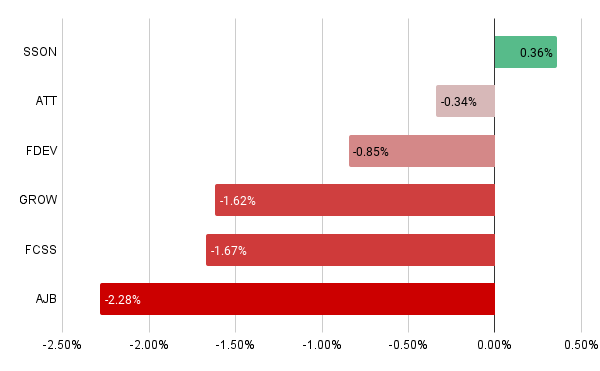

The biggest detractors to performance were Molten Ventures, AJ Bell, and Fidelity China Special Situations, all acquired in the first week of January before the wider sell off began to gather pace. The return contributions from each of the holdings are shown below:

Some big falls for those early purchases in the first quarter then, but perhaps some evidence that sentiment is beginning to improve. Early March proved to be the bottom for the quarter for both the portfolio and the benchmark. Since then the MIA Sentiment Index has risen for 4 consecutive weeks, moving out of the ‘Fear’ range and is now back at ‘Neutral’. Will this trend continue into Q2? Anything could happen.

Hope you enjoyed this update and thanks for reading.

This article is intended for informational purposes only. It is not a recommendation to buy or sell shares or other investments. Always do your own research before buying or selling any investment or seek professional financial advice.