Saietta Group

Saietta Group looks interesting.

It is interesting because it has an innovative product. It is interesting because its product has a massive potential market, and it is interesting because of the strategic way that it intends to tap into that market.

Innovation

Saietta, has developed a low cost, high efficiency electric motor that can be used to power many different kinds of vehicles. The special feature is that combination of low cost and high efficiency. It is special because of the impact that it could have on the overall price of the electric vehicle especially when you also consider the battery required to power it. High efficiency motors convert more electrical energy into kinetic energy than lower efficiency motors and therefore require smaller, less expensive batteries to travel an equivalent range, but the motors themselves are usually more expensive. As such, the use of a higher or a lower efficiency motor has previously had little impact on the overall cost of electric vehicles. This is what the company calls the ‘EV Paradox‘ which they say their product has solved and is key to opening up the EV market. From Saietta’s 2021 AIM admission document:

The Directors believe that being able to reduce power unit size, weight and cost is an important focus for automotive OEMs and by achieving that, the Company will further support and accelerate the mass market adoption of electric vehicles.

Advances in battery technology are another driver of EV market adoption. Batteries are becoming less expensive which in turn is reducing the cost of electric vehicles relative to internal combustion engine (ICE) vehicles. The development of swappable batteries is another advance that has the potential to reduce prices further and opens up the possibility of consumers leasing batteries rather than buying them with the vehicle. Instead of having to spend time recharging, vehicle owners would be able to simply swap out depleted batteries at a network of stations - an idea that is already being implemented in Taiwan.

The Group is taking steps to protect its motor design through a number of international patents, and intends to capitalise on the shift to electric vehicles in the automotive industry:

The Board believes that these changes provide material opportunities for new entrants and that there are currently no direct competitors to Saietta’s AFT 110 or 140 motors for its target market, with no other motor having the same unique combination of attributes allowing for low-cost manufacturing with comparable performance attributes.

Market Opportunity

The target market referred to in the quote above is not electric cars as you might expect, it’s electric motorcycles (which are part of the broader 'L Category’ or ‘lightweight mobility market‘). It’s a big market. Global sales of electric motorcycles have already reached 17 million per annum, and are forecast to reach 39 million by 20301, growing at a faster rate than passenger vehicle sales. This is where the company sees its opportunity:

The Directors believe the performance and cost required from traction motors for electric L Category vehicles is not well served by the current electric motor providers and that Saietta’s innovative AFT topology should have a clear competitive advantage.

The largest motorcycle markets in the world are in Asia and Saietta is initially targeting India, the world’s largest market, where more than 20 million motorbikes are sold annually. Around 65% of sales in India are in the 100-165cc range where (at the time of the admission document) the company sees little or no competition:

The Directors believe there are no e-motorbikes in the equivalent of the 100-165cc band that have yet been launched, making it an ideal time for Saietta to enter the market.

Competitive Advantage

Saietta’s motor also has a couple of other interesting features that makes it suited to conditions in Asia:

Saietta’s AFT motor delivers a liquid-cooled solution for lower power vehicles on a cost-effective basis, which few other competitors are able to currently do.

This might prove to be a significant competitive advantage against its air cooled competitors in warm Asian climates and in areas with high levels of traffic congestion:

The high temperatures and low speed airflow in slow moving traffic makes cooling air-cooled motors a significant challenge.

Saietta says that its motor also has higher torque than its competitors in the Asian market. The implication here is that the Saietta motor will have better performance when pulling away from a standing start - another useful feature in congested traffic.

A Faster Route To Market

Getting a foothold in the automotive industry in Asia will take some time, and will depend, among other things, on the pace of infrastructure roll out to support the mass adoption of electric vehicles.

In the meantime Saietta has another plan to achieve initial sales more rapidly - outboard motors for use on Europe’s inland waterways, where regulation is forcing an imminent switch to electric powered units:

…there are over 12,000 private inland vessels in the city of Amsterdam and currently approximately 95% are powered by ICE outboard motors. These petrol and diesel outboards have been banned in Amsterdam city centre from 2025 and, as yet, there are few viable functioning products to replace them.

Figures from the admission document suggest that Saietta’s target addressable market in Europe was ~$18m in 2020 and is predicted to rise to over $300m by 2030 as the adoption of electric motors accelerates.

The Strategy

The rapid technological change that’s driving the seismic shift from ICE vehicles to EV, is Saietta’s window of opportunity, but the pace of change is such that there is a need to move quickly to mitigate the very real risk of its products becoming obsolete before they are able to gain traction in their target markets.

Saietta though is a small company with a limited track record of commercialising its technology. To be taken seriously the company needs to be able to prove its technology’s viability, find the right partnerships to give it access to mass markets, and have the right business model to be able to capitalise. The strategy has four main strands:

Provide research, engineering design, and testing services to integrate its motors into clients’ vehicles. This area is already revenue generating.

Build a production facility in the UK with capacity to produce 100,000 units per annum that will demonstrate the product’s suitability for low cost mass production.

License the technology so that major customers can establish their own manufacturing capability using the UK production facility as a model.

Provide test certification through a new Motor Durability Test Centre being built in the UK.

Operational Progress

Saietta’s HY21 interim results provided an update on progress. Cash raised from the IPO is being spent on the new UK test and production facilities with the production facility due to open at reduced capacity in Summer 2022. Saietta has also secured additional production capacity by taking on an existing manufacturing facility in Sunderland, which means the company will be able to reach its target of 100,000 units per annum “significantly ahead of its target and budget at the time of IPO“. As part of the deal Saietta will also take on 39 staff from ZF Automotive UK which previously operated the facility.

A new joint venture that will be key to accessing the Indian motorcycle market has been finalised with Padmini, a specialist manufacturer and distributor of automotive parts to some of the biggest motorcycle manufacturers in the region such as Hero (6m units per year) and TVS (2.4m units per year). Prototype motorcycles fitted with Saietta motors have also been built and shipped to India for evaluation.

In November 2021 the company launched its first electric outboard (and inboard) motors at a marine trade show under the ’Propel’ brand securing orders of £0.9m and effectively selling out for the next 12 months.

Acquisition of e-Traction

There has also been the unexpected acquisition of e-Traction, a similar company to Saietta, from Evergrande (yes, that Evergrande), doubling Saietta’s headcount. Evergrande’s debt situation looks to have been to Saietta’s advantage, acquiring e-Traction for an initial consideration of just one Euro and a further €2m (funded from cash raised by the IPO) on the basis of:

certain conditions being achieved by the Seller with regards to approvals from the relevant agencies of the People's Republic of China.

e-Traction generated revenue of €1.2m in 2020 but that looks to have been severely impacted by a reluctance of clients to place orders due to Evergrande’s debt situation. The previous year e-Traction generated revenue of €11.4m. Saietta also acquired e-Traction debt free with Evergrande waiving €21m of loans it had made to the company.

The acquisition extends Saietta’s immediate markets to include commercial passenger vehicles (buses) including a retro fit solution, but perhaps more strategically important is e-Traction’s expertise in power electronics, and its production facility for inverters - key components that are used to control the speed and torque of electric motors.

Future Potential

There can be no doubt that the move to electric vehicles is underway, creating a massive, but highly competitive, market opportunity for those companies with the right product and commercial skills to capitalise.

Saietta’s management does have significant experience in the automotive industry. The CEO, Mr Wicher Kist has an engineering background with Cosworth and was CTO at Dutch supercar brand Spyker. The Chairman, Mr Anthony Gott was formerly CEO and Chairman at Rolls Royce. The admission document also says:

Both the Board and the senior management team include leadership and technical expertise with successful track records in the commercialisation of innovative design

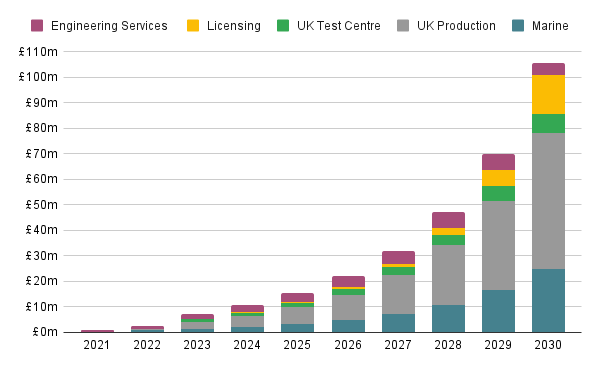

If the company is successfully able to execute its strategy, revenue could ramp up significantly over the next few years to more than £100m. The chart below illustrates the potential based on figures extracted from the admission document2:

The projections look impressive, but are the leadership backing themselves, and have they manged to convince anyone else to back them? Saietta’s biggest investor is Emmanuel Clair, a non executive director with a 14.8% holding. The CEO, Wicher Kist, currently has a 1.5% stake in the company.

The Group has also attracted external backing from Amati Global Investors which has an 11% holding, and from Premier Miton which owns 8%. Saietta is currently the largest holding in the Premier Miton UK Smaller Companies fund.

Saietta then, has a product with the potential to sell millions of units, in a market undergoing huge transformation. But many things could go wrong and for the next couple of years Saietta will be burning cash as it builds out its new facilities. The AIM admission document also noted that more money will be needed:

…the Company will require further funding in addition to the net proceeds of the Placing in order to complete the construction of the Pilot Production Factory

A lot has happened since that statement, with IPO funds being used for the unplanned acquisition of e-Traction and an additional manufacturing facility.

Saietta will come up against bigger competitors developing similar products who have more resources to plough into R&D. It remains to be seen how much protection from competitors will be provided by the patents on Saietta’s motors. The admission document also noted additional patent risk in some markets:

there is a real but low risk of the Company infringing third party patent rights in relation to the commercialisation of the AFT in China, the US and Japan

Perhaps an indication of how things might play out is the recent acquisition of Oxford based competitor Yasa Ltd by Mercedes-Benz. This is clearly a scenario that is on Mr Kist’s mind. In the recent interim results investor presentation Mr Kist said that he hoped Saietta would stay independent for “as long as possible”.

What is certain is that we are about to see huge demand for electric vehicle technology. The market is likely to become fragmented as it supports new entrants bringing the latest technologies, followed by consolidation involving the big automotive manufacturers. The Yasa example is an indication that this is already beginning to happen. How long might a successful small independent be able to stay independent in this environment?

Saietta is a company to watch.

This article is intended for informational purposes only. It is not a recommendation to buy or sell shares or other investments. Always do your own research before buying or selling any investment or seek professional financial advice.

According to the 2020 Bloomberg New Energy Finance (BNEF) Report.

Marine: Saietta is targeting at least 10,000 electric outboard motors per annum with a potential wholesale revenue of £2,500 per motor, implying revenue of £25m by 2030.

UK Production: The Group targets a blended average revenue of £783 per unit from its directly manufactured motors. Full capacity of 100,000 units implies potential revenue of £78.3m (£53.3m excluding marine).

Licensing: A 2.3% market share of an estimated 65m global electric motor sales in 2030 could equate to 1.5m Saietta motors being manufactured under license with a target royalty of £10 per motor implying revenue of £15m.

UK Test Centre: Expected to be operational from late 2021, with target capacity of 20 test cells each generating £1500 of revenue per day implying annual revenue of ~£7.5m.

Engineering Services: Assumes gradual reduction in engineering services as a percentage of total revenue as production and licensing deals ramp up.